NATIONAL Foods Limited (Natfoods) is one of the oldest and biggest groceries manufacturers in the country. With a history stretching from 1908, the manufacturing giant owns and operates some of the household brands like Gloria flour, Red Seal and Pearlenta.

Its product portfolio ranges from flour, mealie meal and pasta to biscuits, snacks and cereals.

The company has also a subsidiary that owns properties that are leased out to its business units.

Based on its industry and type of business, Natfoods is one of the companies whose performance in a given year is largely influenced by the rainfall.

It uses agricultural inputs like cereal crops in its manufacturing and it does this by utilising contract farming. It prides itself as the biggest off-taker of the “A Growth” contract farming scheme in the country.

Its financial year, which runs from 1 July to 31 June coincided with the El Niño-induced drought that affected Zimbabwe and other countries in the region.

Naturally, one would expect a company like Natfoods, holding other things constant, to be adversely affected by this natural disaster.

Nevertheless, the company still managed to post a 6% growth in its sales volumes.

- NatFoods loses US$162K to internal burglars

- National Foods revenue seen at US$302,5m

- National Foods pays dividend to employees

- National Foods empowers rural youth

Keep Reading

As a manufacturer of basic goods, it also has a tendency to perform well or at least above average in periods of economic turmoil. Its defensive nature allows it to continue recording sales volume as economic agents cut on more discretionary spending and stick to basics.

Was this the case in FY24? Let us find out. According to the chairperson’s statement, which accompanied the FY24 results, Natfoods faced a number of challenges during the year above just the drought.

In fact, the drought was mitigated by the fact that South Africa had a buffer, and the group was able to import from South Africa to cover the gap.

The drought may to some extent have worked in favour of Natfoods in the sense that they witnessed a 21% growth in the maize milling division. This growth, according to the group, was attributed to lower local maize harvest which meant that most households had reduced stock.

The buoyant overall volume performance also came from the growth in the snacks unit of the business. This division manufactures and sells products like the ZapNax, King Kurls and Allegroes.

Snacks witnessed a 45% growth in volumes, and this was mainly spearheaded by capacity enhancement measures taken by the group.

The stockfeed division also registered an 8% growth at the back of the poultry category. The cereals division where brands like Nutri Active, which was launched in 2021, recorded another 8% growth rate.

There are divisions, which performed below expectations, and these include the biscuits and down-packing divisions. The biscuits division, where the Iris biscuits fall under recorded a 23% decline in volume.

Natfoods commissioned a new biscuit production line, but this was posted after the reporting period. In the FY25 we are likely to see an improvement in the biscuits unit given the increased capacity. The down-packing division also saw a 21% decline in volumes. This unit packages product like rice and salt and the decline in volume was after India imposed a ban on rice exports.

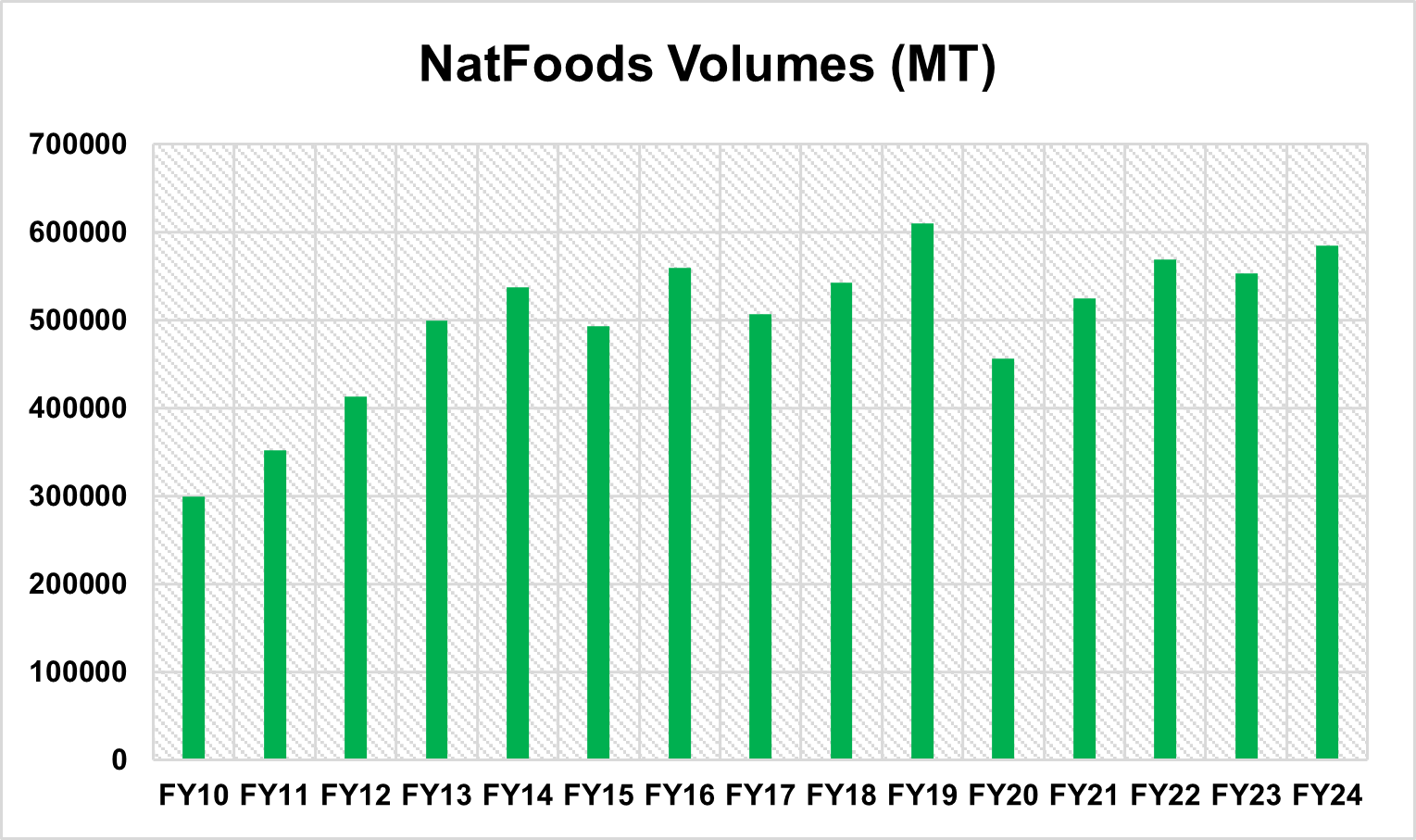

Overall Natfoods have steadily grown its volumes over the past decade, despite the growth not being the smoothest. They are yet to get back to the record volumes recorded in FY19, above 600 000 metric tons.

Interestingly, Zimbabwe also faced a drought in the 2018/19 agriculture season which coincided with Natfoods’ FY19 numbers.

Reading along the company’s financials one gets the sense that Natfoods was impacted more by other things than just the drought.

These include the change in the tax law. Earlier in the year, Value Added Tax (VAT) on some basic commodities including maize meal and floor amongst others was changed from zero-rated to exempt.

This means that Natfoods was not able to claim tax input credits against these goods resulting in a 6% increase in its monthly operating costs.

As a manufacturer, the other challenge Natfoods faced was the pricing distortions on the route to market. Due to currency and exchange rate issues that are affecting the market, there has been a shift by consumers to more informal retailers, at the expense of the formal ones which are required to adhere to using official exchange rates.

This challenge is not peculiar to Natfoods only, but most food manufacturers and we have witnessed companies like Dairibord try to come up with ways to control that route to market.

From a financial analysis perspective, Natfoods saw top-line growth of 5% in line with the 6% growth in sales volume. The group reported a gross profit margin of 22,7%, a slight improvement from FY23’s margin of 21%. At the net profit margin level, the FY24 was way higher at 3,8% versus the comparable period at 2,19%, this was mainly due to a reduction in financial loss to financial gain between the two periods.

At earnings per share of USc20,11 the group is currently trading at a twelve-month-trailing price-to-earnings ratio of 9,47X. Innscor, which is a shareholder in Natfoods, but also a food manufacturer, amongst other things, is currently trading at 6,78X. Natfoods paid a dividend of USc3,29 per share, taking the full-year dividend to USc6,71 per share.

This translates to an annual dividend yield of 3,5%. The dividend yield for Innscor was 6,5% whilst Simbisa was 2,98%.

From a cash flow perspective, the group’s cash flow position improved by 101% during the financial year. The increase in the net cash flow position was mainly spearheaded by the increase in the cash-flows from operations. The company has been investing to increase its capacity and has US$8 million in approved but not yet contracted capital expenditure.

However, in FY24 the company deployed about 18,5% less capital expenditure than it did in FY23.

In conclusion, Natfoods managed to survive and post positive numbers despite the drought experienced in the year. It managed to grow the sales volume and both the top and bottom-line.

The company is also affected by other economic factors mainly influenced by government policy and has to deal with the effects of those besides just natural disasters.

Hozheri is an investment analyst with an interest in sharing opinions on capital markets performance, the economy and international trade, among other areas. He holds a B. Com in Finance and is progressing well with the CFA programme. — 0784 707 653 and Rufaro Hozheri is his username for all social media platforms.